Saving to a Traditional IRA versus a Roth IRA is a common question that comes up and like many questions it usually starts with “it depends” as there are pros and cons to each…Sorry you must read more!

The contribution limits are the same for both, $6,000 per year maximum and you can contribute to one or a combination of the two with the cumulative maximum of $6,000 and an extra $1,000 totaling $7,000 if you are over age 50. You can start a Roth or IRA for kids as early as you’d like as long as the kiddos have earned income and highly recommend the Roth for kids, more to come on this later.

You must have earned income for the calendar year you contribute of that earned amount or greater. This must be W-2 job income, so the income can’t be from a pension, social security or other sources. Your income and whether you have a workplace plan available to you will determine your eligibility. Assuming there is earned income, everyone is eligible to make an IRA contribution no matter what. The question then becomes whether the IRA contribution is deductible and that is determined by answering 2 questions:

• How much is my adjusted gross income (AGI)?

• Am I covered by a workplace plan?

If you are only contributing to the IRA to get the tax-deduction, then you will want to make sure your income is below these figures. For those who do not have a workplace plan to contribute to, there is an income limit to get that deduction and the limit comes down even further if you are covered by a plan at work.

As a brief aside, many clients ask a great question “how does this contribution go in pre-tax into the IRA if I’m making the contribution from my bank account where I already paid the taxes?” Yes, you make the contribution with those after-tax dollars, but the IRS then reduces your taxable income from as an example, $50,000 for the year to $44,000. This allows the $6,000 amount to be excluded from income taxes making it “pre-tax” since that is income from your job that you don’t have to pay taxes on once your tax return is completed.

Speaking of the tax-deduction, often times folks look to the IRA for a tax deduction but have not maxed out their 401k, 403b, 457 plans at work. Workplace plans are much more straightforward and often the best first option for retirement savings. There are no income limits at all within these plans. An individual could hypothetically earn over $1 million per year, and they would still be eligible for the tax deduction of $19,500 if under 50 years old and $26,500 if over age 50. If you are looking for tax deductions and wondering about an IRA, I would first make sure you are maxing out the workplace plan.

If you are maxing out the workplace plan and make over the income thresholds, you can still make an IRA contribution, however the IRS will not give a tax deduction to do so. One thing to keep in mind is if you have other pre-tax IRA assets and you are considering an after-tax contribution, I recommend taking a pause and speak with a financial professional to discuss the ramifications. The IRS allows it, but it will make tracking the sources of pre and post-tax funds quite the project and when it comes time to withdraw from these accounts and the burden is on you to prove to the IRS that you already paid taxes on a portion of the funds. If you do decide to move forward with that strategy, I would recommend putting a contribution like that into a separate, IRA to help track things. However, when you withdraw from the accounts down the road, the IRS view withdrawals as one big IRA and there is a pro-rata formula used which again, is a bit complicated. For example, the IRS doesn’t allow you to withdraw from the “after-tax IRA” account you have had segregated for all those years.

Unlike the IRA, the Roth has income limits that if you earn over the limits you are not eligible to contribute to the Roth at all. The Roth contributions go in post-tax with no tax-deduction but once those funds are in the Roth they grow tax-free forever never to be taxed again. The power of compounding interest which is growth of your growth in the account is most powerful over longer periods of time thus making the Roth much more beneficial for younger folks, especially kids! If you want to help your kids, teach them about money and get them a head start in life, the Roth contribution on their behalf is an incredibly powerful and overlooked strategy. A 15-year-old child that earns $6,000 per year waiting tables is a great example of gifting strategy parents can make a full $6,000 contribution to a Roth on her behalf. The tax deduction of the traditional IRA doesn’t mean much to her anyway because the income is low and the money will never be taxed again, ever.

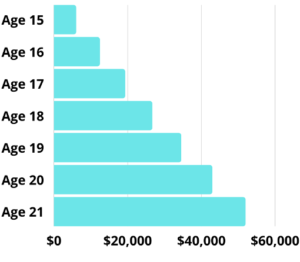

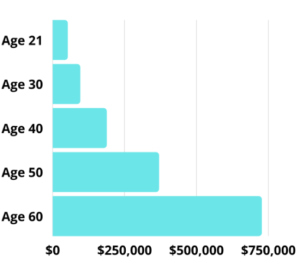

The chart above shows growth of $6,000 annual contributions from age 15 to 21 equals a total gift of $42,000. This would grow to $51,924 by the age of 21 which to start with doesn’t get anyone too excited. However, if the child let this account grow at 7% per year in the Roth IRA and never added another penny the balance, it would grow to $726,667 on her 60th birthday! All that growth ($684,667 to be exact) would be tax free upon withdrawal.

The power of starting to invest early and allowing your money to work for you is much more powerful than saving more later in life. For an individual that delays investing until age 40 and aims to have that amount by age 60 would have to invest $17,725 every single year for 20 years to get to that same balance by age 60! This late starter would have invested a total of $354,500 compared to the $42,000.

Many people want to help their kids but afraid to entitle them and this is a great way to do that since the money is subject to withdrawal penalties until after they are 59.5 years old. If you are already doing some type of gifting strategy directly to kids or grandkids and they have earned income, then this strategy worth considering as an alternative. 529 college savings plans also grow tax-free if used for college, so that is worth considering as an alternative.

Now that the mechanics and general rules are outlined, you may be asking ok so which one should I do, Roth IRA or Traditional IRA? Here are some factors to consider:

Age

As the example above pointed out the difference in taxation and tax-free growth the Roth provides, generally the younger you are the more it makes sense to contribute to the Roth.

Income

As discussed, your income determines which accounts you can contribute to but another thing to consider is what you expect your income to be going forward. If you are currently eligible to contribute to a Roth IRA but expect your income to go up drastically down the road then it may be worth making the Roth contributions while you can. A young doctor is a great example where she may have some income while in school or shortly out of school, they have much less income than they expect down the road.

If your income lands you in the lowest of tax brackets, then you receive much less of the benefit making a traditional IRA contribution and my advice would be normally to make the Roth contribution regardless of age.

Another thing to consider is your income expectations at the time when you withdraw from these accounts in your 60’s or 70’s. If you expect this to be quite low during the withdrawal period, then you may have less taxes owed on IRA withdrawals than others might at that age. Of course, we don’t know exactly where our income or tax rates will be in the future so that is a moving target that we can only estimate at best. This is a good example of financial planning not being an exact science. Save the best you can to the places that make sense at the time. It can be easy to become paralyzed and delay these decisions but at the end of the day whether you choose a Roth or Traditional IRA won’t make or break your finances. In the example above about the young saver, if that money was saved into a traditional IRA then all of those savings would be taxed upon withdrawals. That would make a huge difference not having those funds pay out tax free but having over $725,000 saved would still be much better off than the person who dwelled over the decisions and never made one.

Diversification of withdrawals in retirement

This is a different spin on diversification. When retirement planning, it’s often-times an added benefit of having different sources of assets. The 3 main categories are

• Non-retirement savings/brokerage assets. These are investment or savings accounts that you have already paid taxes on. There could be some capital gains taxes when selling investments in these accounts which should be considered, but the tax consequences of accessing these funds are usually much less than IRA or 401k withdrawals.

• Pre-tax IRA and workplace plan assets generally get taxed on every penny as they are withdrawn. IRA withdrawals can be delayed entirely until age 72 at which time the IRS forces a percentage to be taken out each year.

• Roth IRA assets as mentioned above are completely free from taxes assuming requirements are met.

As an example, let’s look at an individual Rebecca, she is 62 years old and recently retired currently has no income. However, at age 65 her pension starts paying her monthly and both her and husband Jeff’s social security starts up at 67. As you could imagine, once those 3 income sources kick in there is no looking back for opportunities to be in the lowest income tax bracket. This is a good problem to have, but they should take advantage of taking some modest withdrawals from the taxable retirement accounts during those low-income years from age 62-66. This allows those withdrawals from the retirement account to get taxed at a much lower rate than they likely will be down the line regardless of where tax bracket changes go.

As expense needs come up in retirement, a big part of the planning is how to fund those expenses and which accounts to draw upon. I will spare you all the strategies and details here but like the example above, having multiple sources for withdrawals with differing tax consequences gives individuals more levers to pull on as they try to keep the tax bill as low as possible in retirement. The general rule of thumb for order of withdrawals from accounts in retirement is non-retirement savings first, IRA withdrawals second and save Roth IRA withdrawals for last however there are many caveats, exceptions, and nuances to this order. These strategies should be revisited each year as income and circumstances change.

Risk tolerance

In my opinion, this is the most overlooked factor when discussing this topic of IRA vs. Roth. An individual’s risk tolerance and ability to hold more aggressive investments is something that should be strongly considered. As the growth chart above showed for the young investor that gets incredible benefit in the Roth IRA due to time allowing the assets to grow. Folks that have less time for the funds to grow still could benefit from the Roth but have less time for the account to grow and have earnings compound. Of course, we don’t know what our earnings or growth of the account will be but if you are an individual that does not feel comfortable taking risk and likely to have lower earnings in the account, then the Roth is less beneficial for you. To reiterate, the Roth provides zero tax benefits when making the contribution. The entire benefit is having all growth never to be taxed again. If you are comfortable taking very little risk, the accounts are likely to have lower returns than someone who is willing to ride out wild swings of the market and reaping the benefits of longer-term growth. Lower interest rates in the current environment make it even more difficult for low-risk investors to expect much upside with their accounts. With that said, for younger individuals in their 20’s, 30’s and even 40’s, it likely still makes sense to contribute to the Roth regardless of risk tolerance. If you are a closing in on retirement, on the fence of which to contribute to, and you don’t want to take much risk, then the traditional IRA may likely be a better option to at least capture the current year’s tax deduction.

Most individuals own a combination of both risky and conservative assets across all accounts resulting in a diversified portfolio. I often recommend clients to hold their riskiest assets in the Roth IRA as they are likely to grow more than some of their other more conservative investments and pay no tax on all that growth. If you have a time horizon of 15 years or more before needing Roth IRA money, I typically recommend moving riskier assets to the Roth accounts.

A lot going on for a simple question!

Roth 401k versus Traditional 401k

If your employer allows Roth contributions to your company plan which could be 401k, 403b, 457, etc. then the decision is much clearer cut than all of the income-based rules mentioned earlier. There are no income limitations or income rules at all with workplace plans. The maximum employee contribution limits apply of contributing $19,500/year or $26,500/year if you are over age 50 regardless of income. This can be contributed all to one source (Traditional or Roth) or divided up between the two choices with any split you would like. All of the pro’s and con’s of each are exactly the same when it comes to tax-free growth. No matter your income, you receive a tax deduction for all traditional 401k contributions which takes a lot of the confusion out of the mix. This decision comes down to whether you want the tax deduction of the traditional 401k and also the expected growth and amount of time your assets can grow within the plan.

For younger individuals that are maxing out their plans at work and able to forgo the tax deduction using the Roth 401k, they will have an incredible head start to retirement. If you switch your contributions from regular 401k contributions to Roth 401k contributions you will notice your paycheck gets a bit smaller because you now have those earnings flowing to you first, paying the tax on those earnings, and then going into your Roth 401k account. For that reason, there is some short-term pain that will benefit younger folks quite a bit down the road. It’s worth it youngbloods! Back when I was at the big firm I would always tell the new hires fresh out of college to put their 401k contributions into the Roth version of our retirement plan.

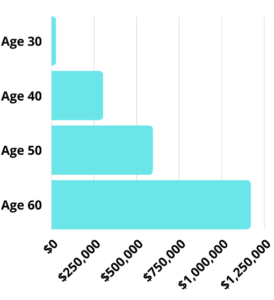

For individuals looking to get as much money into Roth accounts as young as possible they could contribute $19,500 plus another $6,000 (assuming income eligible for the Roth IRA) totaling $25,500 per year saved into Roth accounts! If a 30-year-old did that for 10 years and earned 7% on their investments, total Roth assets would grow to $302,157 by age 40. If that individual stopped investing completely and let those funds continue to grow at 7% inside the Roth until age 60, the balance would grow to $1,169,251! All withdrawals would 100% tax free at that time, not bad for 10 years of savings pain in your 30s…

The same individual making those contributions to traditional 401k and IRA accounts would have the exact same balance at age 60 however at withdrawal time, every single penny withdrawn is added to other income and taxed accordingly. I have had many retirees say that they wish they did more Roth contributions, but to be fair the Roth account is still very young as it was introduced in 1997. In investing as in life, keep doing the best you can. That’s all you can do.